For some important background, make sure you’ve read the first blog post in this series, COGS – Why You Should Care and How to Track It.

This post’s intended audience is distillery management and accountants/CFOs/controllers.

First and foremost, we should define the goal of this exercise. What we’re aiming for is GAAP-compliant books that can be presented to external stakeholders. GAAP-compliant books are not only a good idea, but they are also a regulatory requirement for DSPs (27 CFR 19.73 (11)). An important fact is that GAAP-compliant books do not necessarily provide inventory costs that are accurate down to the product level. Instead, overhead expenses attributed to WIP and Finished Goods inventory need only be accurate in aggregate and in the right period to meet your GAAP requirements for external reporting. In simple terms, GAAP requires overhead costs to be matched to the correct period (vs. the correct inventory unit).

It is a natural desire for management to see accurate, per-SKU costs, including all overhead. These costs (used for business decisions like pricing) should be computed entirely outside of your accounting software and distillery management software. This is referred to as “activity-based costing” (ABC) and it attempts to compute a true cost of production (direct & indirect) for internal decision-making and reporting. For a complete financial picture that serves both external and internal stakeholders, most distilleries will need to compute both GAAP costing and ABC – separately.

As covered in the previous blog post, Material COGS are tracked in your distillery management software. But what about all your other expenses? Some of them are considered non-manufacturing expenses, like Selling, General and Administrative Costs (SG&A) – this includes office salaries, salesperson commission and compensation, advertising, trade shows, accountants and IT, legal and consulting fees and more. SG&A expenses are not considered manufacturing overhead; you simply account for them in your accounting system under SG&A.

In contrast, manufacturing expenses include manufacturing labor, costs of input materials, depreciation of equipment, excise tax, product-related insurance, waste/scrap, subscriptions, repairs/maintenance including consumables and parts, and items like pallets or slip sheets. Some of these costs (e.g. input materials) are direct costs, tracked in your distillery management system as Material COGS and Excise Tax COGS. The remainder are indirect (overhead) costs.

If you are using Whiskey Systems’ labor cost tracking feature, then you can separate out Direct Labor (which is rolled into Material COGS) and Indirect Labor (which is not, and must be accounted for as overhead). If you are not using the labor cost tracking feature, simply account for all your manufacturing labor as indirect labor.

The reality of small to medium distilleries is that individuals typically perform many different tasks across many business functions. Plus, distilleries are usually equipment-, utility- and rent-intensive operations. Given these facts, it is appropriate to avoid the “direct labor” allocation method and use the “machine hours” method, instead.

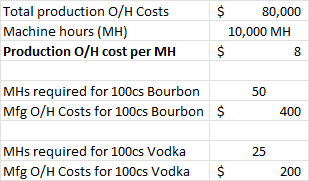

Here’s a simple example of a distillery using the “machine hours” overhead allocation method:

With this method, you define a distillery-wide “machine hour” capacity (instead of direct labor hours) and then assign machine hours to each finished product. This allows you to assign overhead costs to your finished product inventory as needed. The upside here is simplicity; the downside is that you have only a single rate for machine hours which may not reflect the diversity of actual costs (e.g. an hour of distillation may have significantly higher overhead costs than an hour of bottling).

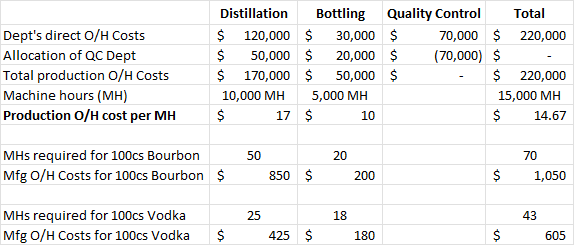

One way to address that is by splitting overhead on a departmental basis. Here’s an example distillery using the “departmental machine hours” overhead allocation method. In this example, we have broken out different manufacturing departments (Distillation & Bottling), as well as a “service” department called Quality Control whose O/H costs are spread across Distillation and Bottling:

Note: For simplicity’s sake, these examples do not include “WIP” inventory, which must also have periodic O/H costs assigned to it under GAAP.

Once you have computed a GAAP-accepted measure of overhead costs, you can proceed to assign those costs to your WIP and Finished Good inventory, at the cadence of your choosing (typically, monthly or quarterly).

Need help navigating these waters? We’re here to cut through the noise and give you actionable, reliable advice. Reach out to our Customer Success team, or book a free Consulting Intro Call.