A bond is a special kind of insurance policy which has three parties, instead of two.

If you think about home or car insurance, you (the policyholder) pay the insurance company a premium, and in the event of a financial loss, the insurance company makes you whole.

A bond (or surety bond) is also an insurance policy, and it also pays out in the event of financial loss. The important distinction is that the beneficiary is a 3rd party (not the policyholder).

Putting this into distillery terms: distilleries maintain surety bond coverage, purchased from an insurance provider, with the US Treasury listed as the beneficiary. This allows the government to protect its interest in excise tax that has been attached to spirits, but not yet paid/collected. In the event of a disaster or if the proprietor defaults on their obligations to pay excise tax, the government will be made whole by the insurance company.

If you cannot or do not wish to obtain a bond, you can also pledge cash collateral in lieu (check or money order). But you might as well earn some returns on your cash – you can also purchase Treasury Notes or Treasury Bills and pledge them as security in lieu of a bond.

Some states also require bond coverage for similar reasons; if you are in a state that requires a bond, you’ll potentially need two separate bonds (one for the State and one for the Feds). Each state has its own requirements, and there are some interesting scenarios – for example, North Carolina requires you to extend your Federal permit and bond to cover products held in their Control State Warehouse.

Up until 2017, all distilleries in the US were required to maintain bond coverage, in an amount proportional to the type and scale of operations (see 27 CFR 19.166). Fortunately, in 2017, the PATH Act created an exception to this rule. If your current and future anticipated tax liability is under $50,000/yr, you are exempt from the requirement to hold a bond! Most craft distilleries fall under this threshold; those operators can stop reading here unless there’s a desire to receive more than 3,700 PGs at a time via Transfer in Bond.

If you are above $50,000/yr in actual or expected tax liability, then you need to know about the various types of bonds specified in the CFR: Unit Bonds, Operations Bonds, Withdrawal Bonds, and Area Operations Bonds. You also need to know that all bonds have a minimum and maximum amount specified in the regulation. If you obtain your bond for the regulatory maximum, you are considered to have “maximum bond coverage” and you can hold & transact an unlimited quantity of spirits. In other words, the requirement to hold a bond “caps out” at a certain level, depending on the type and number of permit(s) that you hold and your withdrawal activities. Full details are in the tables found in 27 CFR 19.166.

An Operations Bond covers the Excise Tax liability attached to the spirits in your Bonded Premises (i.e. distillery operations area), as well as spirits in transit via Transfer In Bond. A Withdrawal Bond covers the Excise Tax liability of spirits during the interim period after they are removed from premises Tax-Determined but before payment of tax has been remitted by the proprietor (otherwise, you’d have to pre-pay your excise tax liability before removing product).

You can simplify matters and obtain a Unit Bond, which is a type of bond that covers both Operations and Withdrawals; you simply add up the separate bond amounts required under Operations and Withdrawals to determine the needed Unit Bond coverage.

Finally, if you have multiple DSPs, then you have multiple bond coverage options. You can treat each DSP as its own entity with its own coverage, which increases costs but also gives some flexibility. You can obtain a single Unit Bond covering both Operations and Withdrawals at multiple DSPs. Finally, you can also obtain an Area Operations Bond and a Withdrawal Bond for multiple plants, covering those operations separately but for multiple DSPs.

Bonds can be expensive and challenging to obtain. You don’t want to buy too much coverage, but at the same time, it’s wise to plan for the future and avoid having to re-buy or strengthen your bond with increased coverage later on.

A final caveat: your Operations Bond covers spirit transferred In-Bond from other distilleries while it is in transit to your DSP. When computing your needed coverage for TIB receipts, you must use the full $13.50/PG tax rate, even if you are entitled to a lower rate for removals under CBMA provisions. In other words, a DSP that has no bond coverage under the PATH Act is limited to having $50,000 / $13.50 = 3,703 PGs in transit at any given time. Roughly speaking, this amounts to seven IBC totes of 190 proof GNS, or 58 barrels of MGP Whiskey (approximately one truckload, unpalletized).

If you wish to receive a tanker quantity of 190pf GNS (e.g. 6500 wine gallons or 12,350 proof gallons) then you simply multiply 12,350 * $13.50 = $166,725. This is the minimum amount of Operations Bond coverage you would need to receive that tanker, legally, but that assumes you have 0 PGs on hand in bonded space. A typical DSP’s statutory maximum Operations Bond coverage is $250,000, making this a great example of a situation where it might make business sense to just buy the maximum coverage, instead (then you can have as much TIB spirit in transit as you wish, and store as much as you wish).

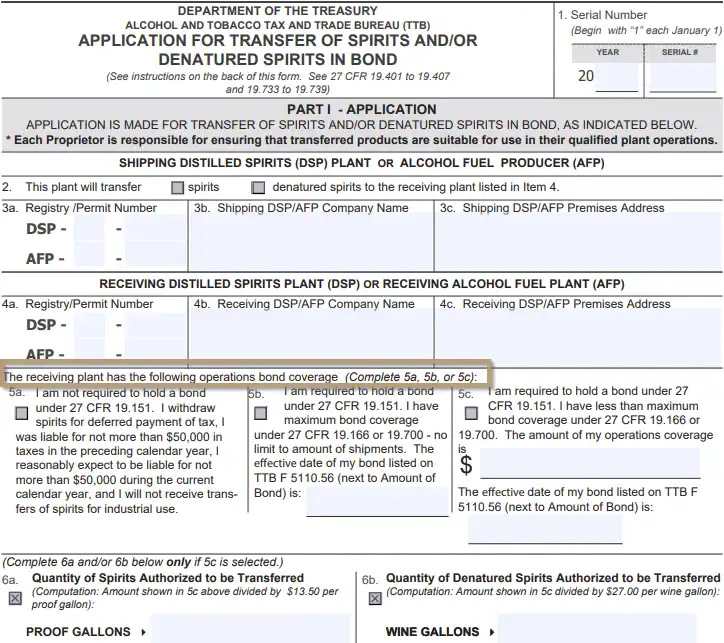

If you ever wondered why the TTB requires you to file a permit amendment & Application for Transfer of Spirits in Bond, you now understand one of the reasons. They must interrogate your bond coverage so that they can convey your “maximum allowed PGs in transit” to the sending DSP. Items 5a,b,c and 6a,b on the Application for Transfer of Spirits in Bond include this information:

Need a helping hand? Book a free call with FIVE x 5 Consulting to get detailed, actionable guidance from the pros.