As we wrap up a dynamic 2024, it’s wise to take a moment to reflect on some common TTB audit findings. Avoiding these pitfalls can save you significant time and expense – and you’re required to follow all the regulations, anyway!

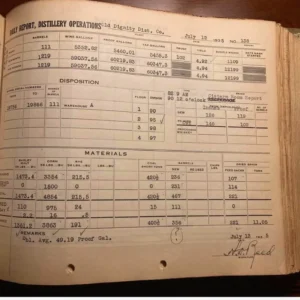

1. Incomplete Gauge Records

TTB regulations require you to gauge your spirit at various points in your production process: when you produce or process spirit, transfer it, add water or other materials, and immediately before bottling. Depending on whether the gauge will be used for tax determination, the required precision and instrumentation can vary. A complete gauge record includes the elements of the gauge (e.g. inches and gallons per inch if gauging volumetrically, or pounds if gauging by weight). You’ll also want to include any calibration offsets used on your hydrometer and thermometer (even if 0). See 27 CFR 19.618 for details.

2. Missing or Incomplete Physical Inventory Records

Distillery Proprietors have two sets of physical inventory-taking requirements. The results of the physical inventory should be recorded in Physical Inventory Records, which you do not submit/send to TTB but instead retain on site for 3 years.

Twice a year (on June 30th and December 31st), you’re obliged to perform a physical inventory of your Cased (Bottled) Goods on Bonded Premises.

Quarterly (on March 31st, June 30th, September 30th and December 31st), you’re obliged to perform a physical inventory of Tanks (Bulk Spirit) on Bonded Premises, although you may exclude Barrels (packages) in Storage from this inventory.

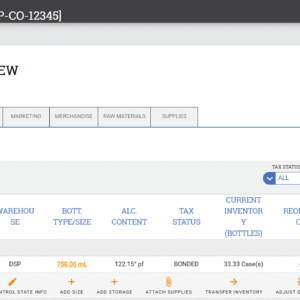

DISTILL x 5 and Whiskey Systems can generate PDFs to assist with this recordkeeping requirement. See more at 27 CFR 19.623.

3. Missing or Incomplete Transfer in Bond Records

Regulations are very specific when it comes to records of Transfer in Bond. Both the shipper (consigner) and receiver (consignee) have inflexible requirements.

The consignee must identify the spirits being transferred, and include the gauge data, package information, spirit age, approved transfer in bond application serial number and date, and much more. Consignee paperwork should be prepared in duplicate; one copy should be physically attached to the shipment (or given to the driver, if sent via bulk conveyance). The other copy should be retained for 3 years. Do not send/submit records to TTB unless requested.

The consignor must validate the shipment against the data on the Transfer Record, notify TTB of discrepancies, and an authorized signer, PoA or officer of the company must sign the “consignee” section of the Transfer Record that the consignor prepared. In this section you must indicate the liquid account that the spirits were deposited into, as well as any variances you have observed. As above, this document must be retained for 3 years but should not be sent into TTB unless they request it.

See more at 27 CFR 19.620 and 19.621.

Hard Copy vs Digital

In general, you are permitted to keep your records in electronic format (e.g. you can scan your completed Transfer in Bond records and maintain only digital copies). The regs simply require that you are able to produce the record in hardcopy format upon request.

If you need help with any of your regulatory requirements, don’t hesitate to book a free intro call with Fx5 Consulting. Our years of expertise can save you time, anguish and money.