“From Bond”, “In Bond”, “Bonded” … it can seem like the regulations are fixated on the concept. But what does it all mean?

First off, some background. In the US, the Federal Government’s Excise Tax attaches to spirits the instant they come into existence (when vapor condenses to liquid). However, to allow proprietors flexibility in producing & storing spirits, Bonded Premises are a special place where Excise Tax liability is deferred, allowing you to produce, manipulate and store your product without having to determine and pay Federal Excise Tax.

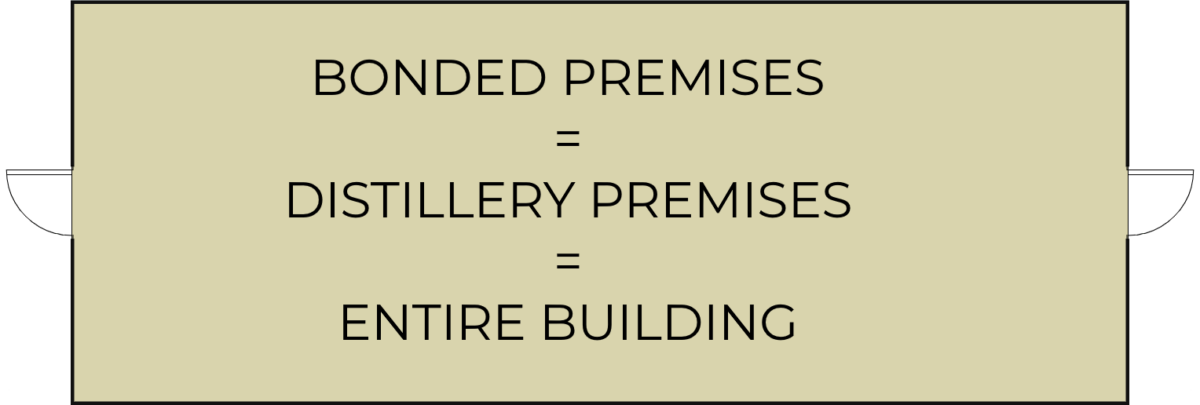

All distilleries in the US have “Bonded Premises”. This is the section of your facility that is covered by your Surety Bond (see also: What is a Bond?). All of your stills, bulk spirits (1 gal+), tanks, production equipment and bottling lines must reside in Bonded Premises – that’s the only place you can legally manufacture, process, store and bottle your untaxpaid spirits.

In the simplest scenario, 100% of your distillery (i.e. the whole building) is Bonded Premises.

However, this configuration can be limiting for a growing distillery. If a wholesaler returns bottled product to your distillery (e.g. due to quality concerns), you cannot store those bottled products in your Bonded Premises because Federal Excise Tax has already been paid (27 CFR 19.58). In this scenario, you also cannot elect to pay Federal Excise Tax on bottles and then sit on them until a later date; you might want to do this because CBMA benefits allow you to take a reduced rate on the first 100,000 proof gallons that you remove (taxpay) in a calendar year.

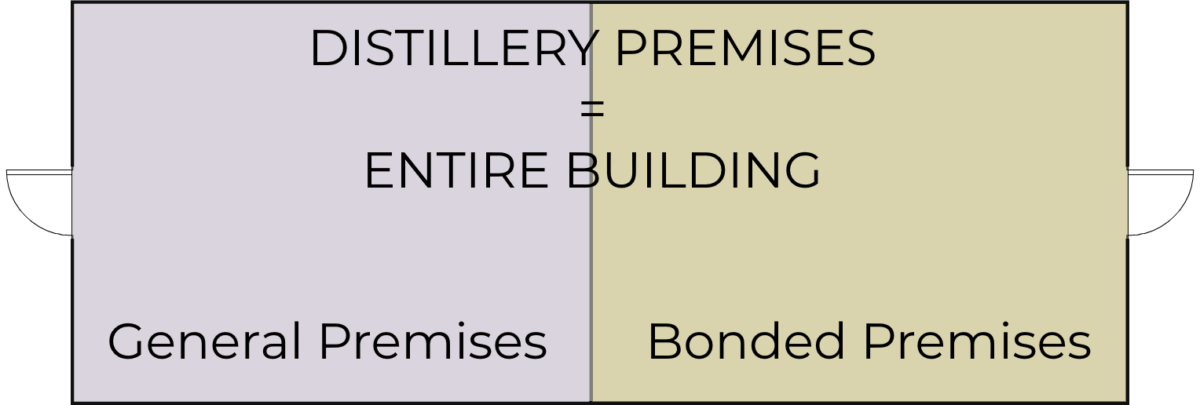

The solution is to add one or more “General Premises” areas to your permit. “General Premises” are also commonly referred to as a “taxpaid area”. TTB’s “Boot Camp for Distillers” webinar defines General Premises as “any business office, service facility, or other part of the premises described in the notice of registration other than bonded premises”. The examples provided for General Premises include: “storage of taxpaid spirits, offices, lunch room, restrooms and non-alcohol storage.”

Your overall Distillery Premises consists of your Bonded Premise(s) plus your General Premise(s), if any. Inside your Distillery Premises, regulations in 27 CFR apply and heavily restrict the operations that you may legally carry out. For example, you cannot produce or sell a nonalcoholic product (under 0.5% ABV) in Bonded or General Premises, unless you have specific permission from TTB to do so in the form of a variance.

Finally, 27 CFR 19.52 contains a prohibition against establishing a Distilled Spirits Plant in a place “where liquors are sold at retail”. Consequently, you may not establish a bottle shop or tasting room anywhere on your Distillery Premises. Remember, your Distillery Premises includes/contains your Bonded Premises and your General Premises. This is an important distinction: many distilleries decide to open a tasting room or bottle shop in their pre-existing General Premises, thinking that it’s allowed because it’s not inside Bonded Premises. This logic is faulty because of the prohibition against retailing on distillery premises.

Let’s see what these scenarios look like in real life, with some simplified floor plans.

Simplest Case – The entire building is Bonded Premises; no General Premises; no Tasting Room:

Now, let’s look at a Distillery Premises that contains both Bonded and General Premises:

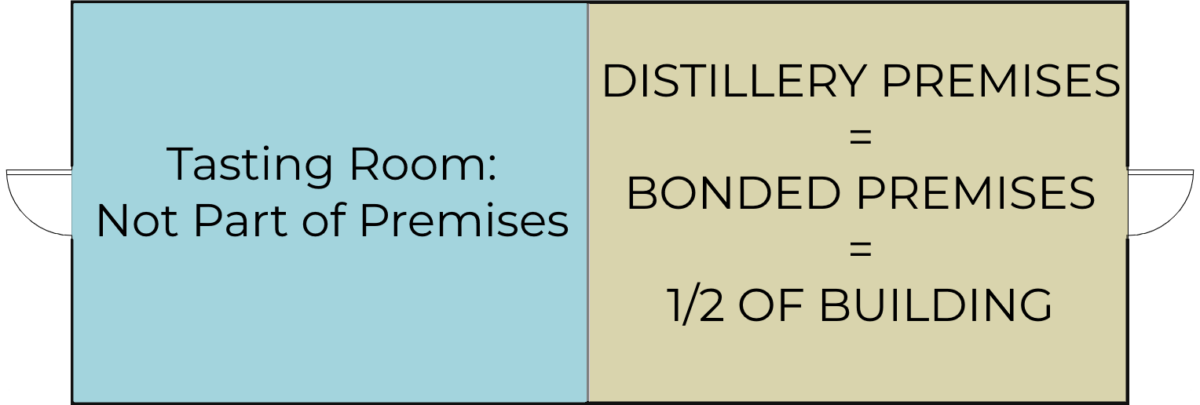

OK, but what if we want a Tasting Room instead of General Premises?

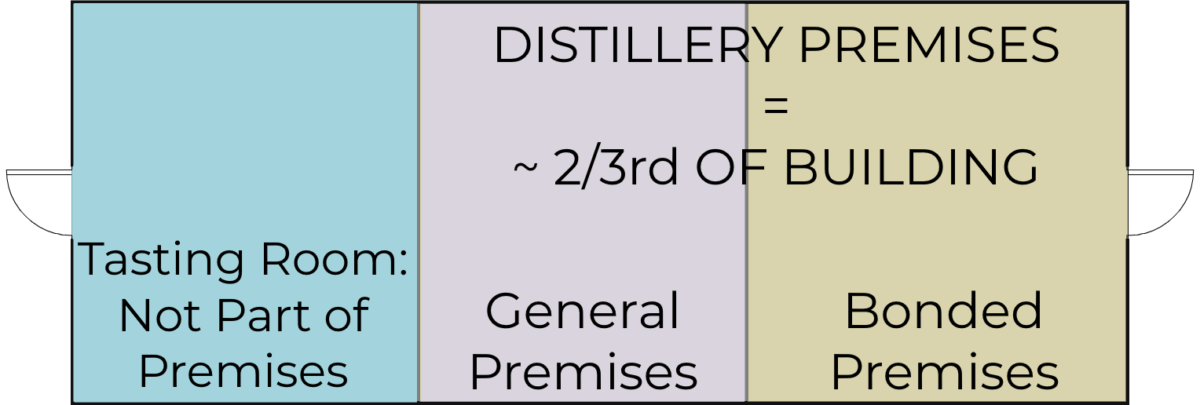

Let’s get complicated. How about a Distillery with Bonded Premises, General Premises, AND a Tasting Room?

As you can see in these examples, you must have a clear understanding of the distinctions between a physical building and the logical distinctions within it for General and Bonded Premises, plus retail areas that are “Not part of premises”. In the simplest case, the physical Building, Distillery Premises and Bonded Premises are all referring to the same space. But if you have a more complicated physical layout, then the distinctions between those terms become very important.

Note also that TTB will require an outside door for direct access to your Distillery Premises. If you are selling bottles, then your retail space (remember, not part of premises) should have its own dedicated exit (door) so that patrons are not bringing taxpaid alcohol into bonded premises when they walk out.